Confronted with the threat of another impending federal government shut-down over the budget, much has been made of recent trends in the dissolution of norms in both politics and civility.

For a longer run perspective on the role of norms, I thought it useful to visit an interesting paper (ungated) in the Journal of Institutional Economics by Peter Calcagno (College of Charleston) and Edward Lopez (Western Carolina University) on the role of informal norms in the federal budget process. The argument is in the title with “Informal Norms Trump Formal Constraints: The Evolution of Fiscal Policy Institutions in the United States.” Here is the abstract:

Two shifts of informal rules occurred in the decades around the turn of the 20th century that continue to shape U.S. fiscal policy outcomes. Spending norms in the electorate shifted to expand the scope of the government budget to promote economic security and macroeconomic stability. Simultaneously, norms for elected office shifted to careerism. Both norms were later codified into formal rules as legislation creating entitlement programs, macroeconomic responsibility, and organizational changes to the fiscal policy process. This institutional evolution increased demand for federal expenditures while creating budgetary commons, thus imparting strong motivations to spend through deficit finance in normal times. Despite the last four decades of legislative attempts to constrain spending relative to taxes, the informal norms have trumped the formal constraints. While the empirical literature on deficits has examined the constraining effects of informal rules, this paper offers a novel treatment of shifting norms as having expansionary effects on deficits.

Here is some more:

Our historical investigation traces today’s U.S. fiscal policy challenges to two shifts of fiscal norms from about 1880 to 1930. First, there emerged new demands on federal spending to support economic security at the household level and economic stability at the macro level. Second, the industrial organization of supplying federal spending became professionalized and competitive, as elected office transformed from a temporary public service to a pursuit of a career ambition. We describe the combination of these two shifts–the demand side spending norm and the supply-side professionalization norm–as the American polity’s shift away from a balanced-budget norm in favor of a deficit-as-policy norm.

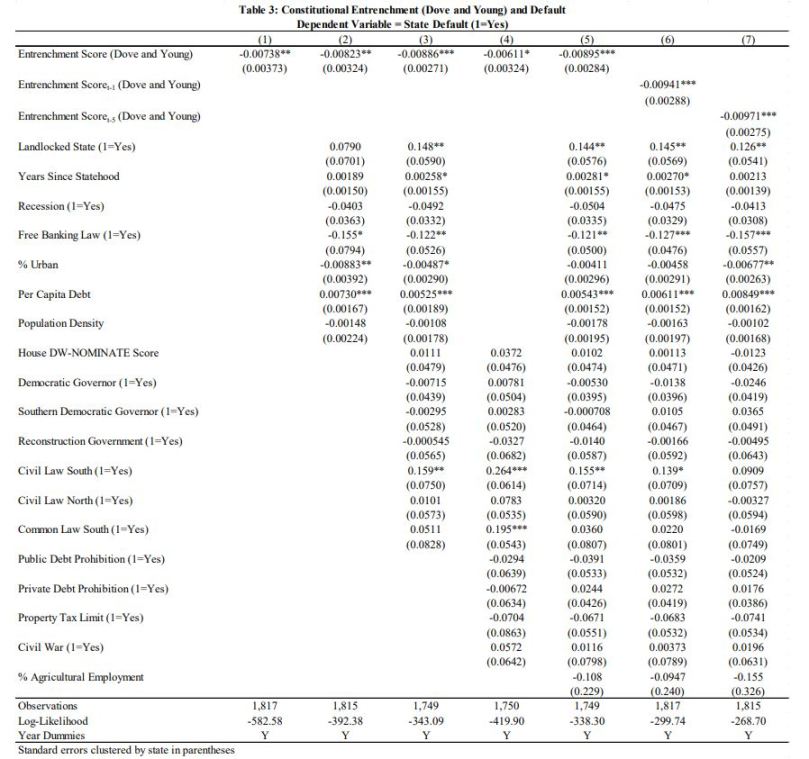

See also a recent blog post here on a paper in Public Choice on the influence of formal rules in state constitutions. It is tempting to see those two as opposing views, but I would be inclined to read it as Calcagno and Lopez arguing that informal rules carry more explanatory power, not that formal rules are irrelevant at the margin.